What works for forecasting macro economic series with deep learning?

Macro data is awkward for deep learning: short history, lots of missing values, mixed frequencies. I ran experiments on Korean output and investment indices with several model families. Below: what the data looks like, what actually worked (and what didn’t), and a few caveats.

What the data is like

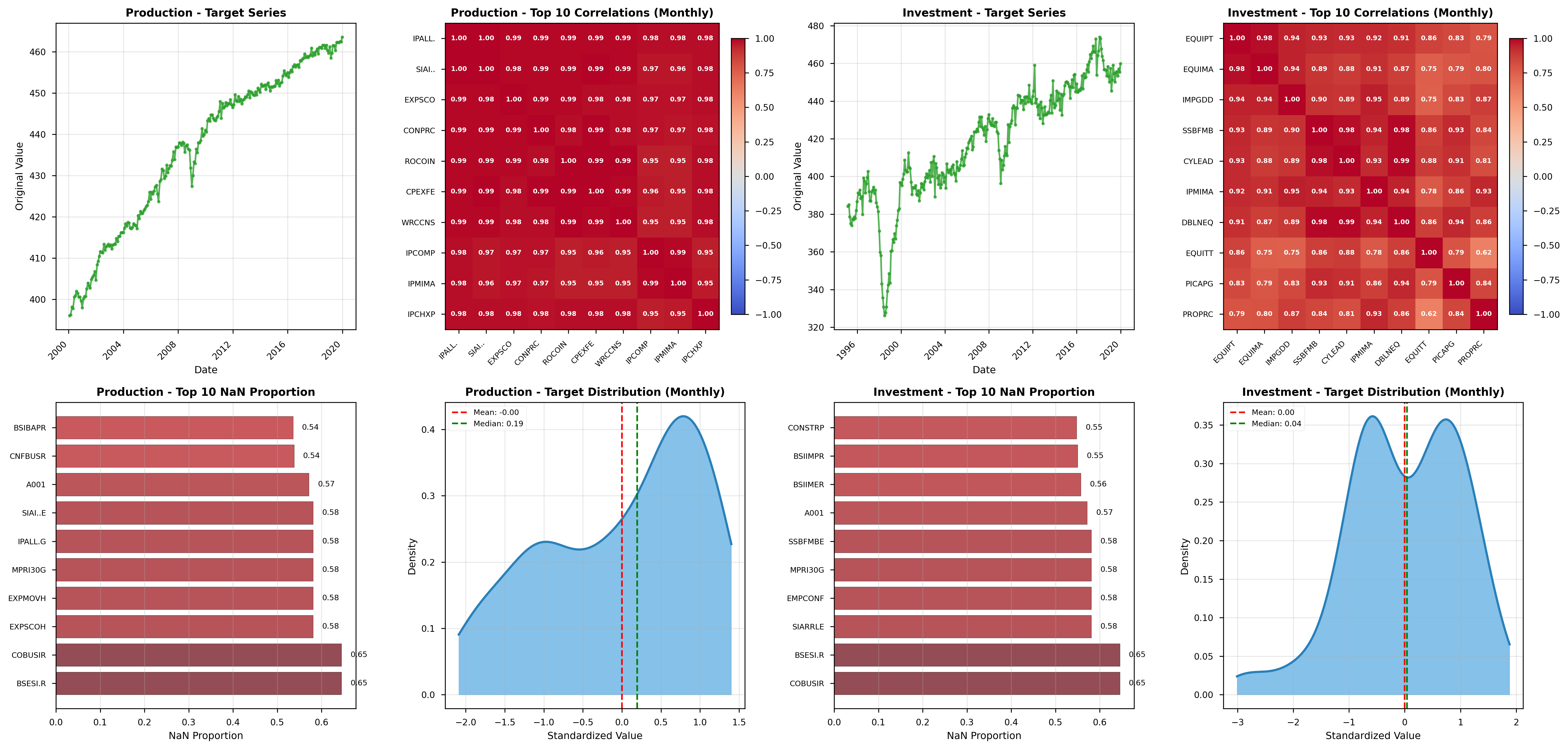

Macro data often has very few time steps—you don’t get decades of daily points. That makes it easy to overfit. The setup I used was a real-time nowcasting pipeline for Korea: dozens of series (employment, prices, surveys, etc.) and two targets: all-industry output and equipment investment.

The series sit at high levels but don’t move much from one period to the next—especially the output index. So there’s limited “signal” for a model to learn from. The variables are highly correlated (a lot of redundancy). Some series are weekly, others monthly, and many values are missing (e.g. data not yet released). Models that can handle missing data “inside” the model (so-called state-space or factor models) have an advantage; others need you to fill in gaps first.

What worked and what didn’t

Bottom line: no single best model. Results depended a lot on which series I was forecasting and how I set things up.

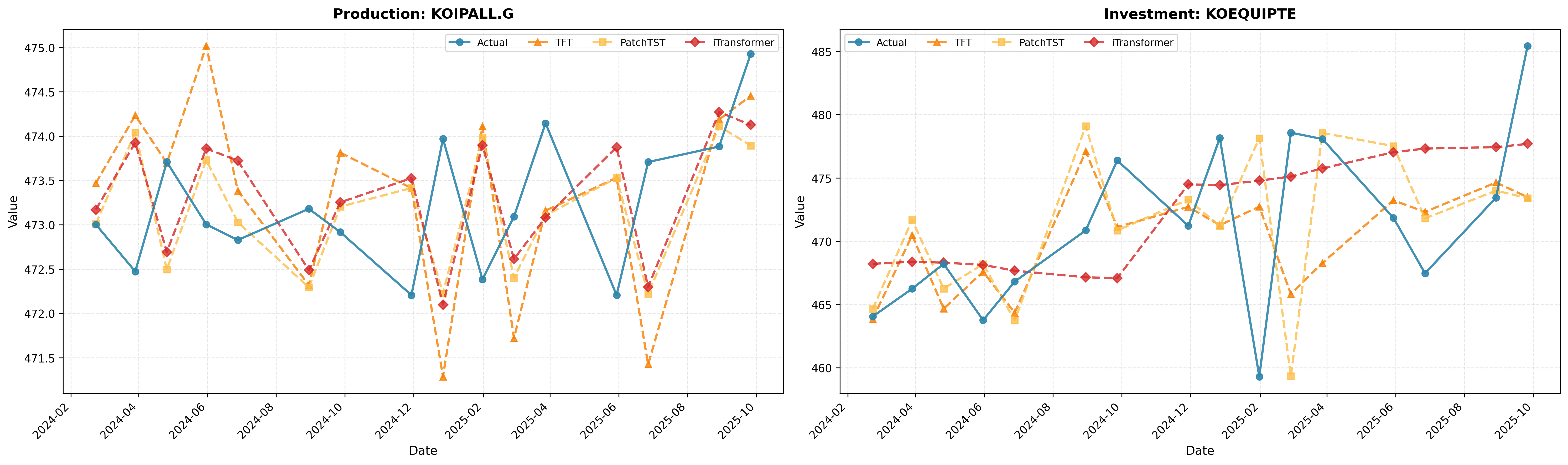

On the output index (flat, low variance, high correlation), a model that mixes weekly and monthly scales (TimeMixer) did poorly—there wasn’t enough variation for that kind of decomposition to help. On investment, which moves more and has clearer weekly–monthly structure, that same model did well. A transformer that looks at relationships between variables (iTransformer) did best on the output index; another patch-based transformer (PatchTST) was strong on some targets but inconsistent. Classic factor models (a few hidden “factors” driving all series) were numerically unstable in my setup—I had to add heavy constraints to get them to converge, which made the “interpretable” factors hard to trust. A deep version of the factor model (neural net instead of linear maps) did better, and switching to spline interpolation helped.

So in practice: pick the model to match the series and the horizon. Models with an internal “state” (state-space / factor style) handle missing data and multi-step forecasting in a consistent way, but for short-term accuracy they didn’t always beat the attention-based models when the data suited the latter. Overfitting was a real issue. For real-time nowcasting, updating the forecast one step at a time beat trying to predict many steps ahead in one go.

Caveats and takeaway

This was one country and one data pipeline. The data are short, so conclusions are limited. Takeaway: performance is conditional—match the model to the target series, how far ahead you forecast, and whether you need interpretability. Prefer one-step-ahead updates for nowcasting.

References

-

FRBNY Nowcast — Bok, B., Caratelli, D., Giannone, D., Sbordone, A., & Tambalotti, A. (2019). The FRBNY Staff Nowcast. Federal Reserve Bank of New York Staff Reports, 897.

-

TFT — Lim, B., Arik, S. Ö., Loeff, N., & Pfister, T. (2021). Temporal Fusion Transformers for Interpretable Multi-horizon Time Series Forecasting. International Journal of Forecasting, 37(4), 1748–1764.

-

PatchTST — Nie, Y., Nguyen, N. H., Sinthong, P., & Kalagnanam, J. (2022). A Time Series is Worth 64 Words: Long-term Forecasting with Transformers. arXiv:2211.14730.

-

iTransformer — Liu, Y., Hu, T., Zhang, H., et al. (2023). iTransformer: Inverted Transformers are Effective for Time Series Forecasting. arXiv:2310.06625.

-

Deep Dynamic Factor Models — Andreini, P., Izzo, C., & Ricco, G. (2020). Deep Dynamic Factor Models. Working Paper (v. May 2023).

-

Dynamic factor models — Stock, J. H., & Watson, M. W. (2016). Dynamic Factor Models, Factor-Augmented VARs, and Structural VARs in Macroeconomics. Handbook of Macroeconomics, 2, 415–525. Elsevier.

Other posts

- Can we really get alpha from market data?

Efficient Market Hypothesis, Micro Alphas, and why probabilistic forecasting matters for turning signals into positions.

- Could multivariate time series have their own representations?

Identifiable innovations, diagonal dynamics, and iVDFM: factor recovery, interventions, and probabilistic forecasting.

- Can we make a more risk-aware portfolio agent from utility theory?

Recursive (Epstein–Zin) utility with Monte Carlo certainty equivalents in PPO/A2C, on Korean ETF splits.

- Effective Bird Sound Classification

Mel spectrograms and EfficientNet for bird sound: why the mel scale helps and how to keep the pipeline simple.

- Creating and Evaluating Synthetic Tabular Data

Sequential synthesis for tabular data, plus three checks: propensity scores, CI overlap, and quasi-identifier risk.